Tesla’s Turbulent Q2: Profit Margins Decline Amid Strategic Changes

Tesla’s profit margin hit a five-year low, missing Wall Street targets due to price cuts and higher AI spending. Despite plans for affordable models by 2025, competition led to fewer deliveries and an 8% drop in shares after hours.

On Tuesday, Tesla reported its lowest profit margin in over five years and fell short of Wall Street earnings targets for the second quarter. This significant drop was largely due to the company’s strategic decision to reduce vehicle prices in an effort to stimulate demand, alongside increased expenditure on artificial intelligence (AI) projects. Despite Tesla’s ambitious plans to launch new, more affordable vehicle models by the first half of 2025, the company acknowledged that these models will not deliver the level of cost reductions initially projected. As a result, Tesla’s stock experienced an 8% decline in after-hours trading following the earnings report.

Thomas Monteiro, a senior analyst at Investing.com, emphasized that Tesla’s investors are now more in need of tangible results than ever before, especially concerning the development of the company’s humanoid robot and Robotaxi projects. The second quarter was particularly turbulent for Tesla, with CEO Elon Musk opting to halt the development of an entirely new, cheaper car model. Instead, Musk chose to focus on less ambitious, lower-cost models and the creation of self-driving taxis. This pivot in strategy was intended to help elevate Tesla’s share price. Additionally, the company made the decision to lay off over 10% of its workforce to manage costs more effectively. Tesla also reported that its profits were negatively impacted by restructuring charges and a rise in operating expenses, largely driven by investments in AI.

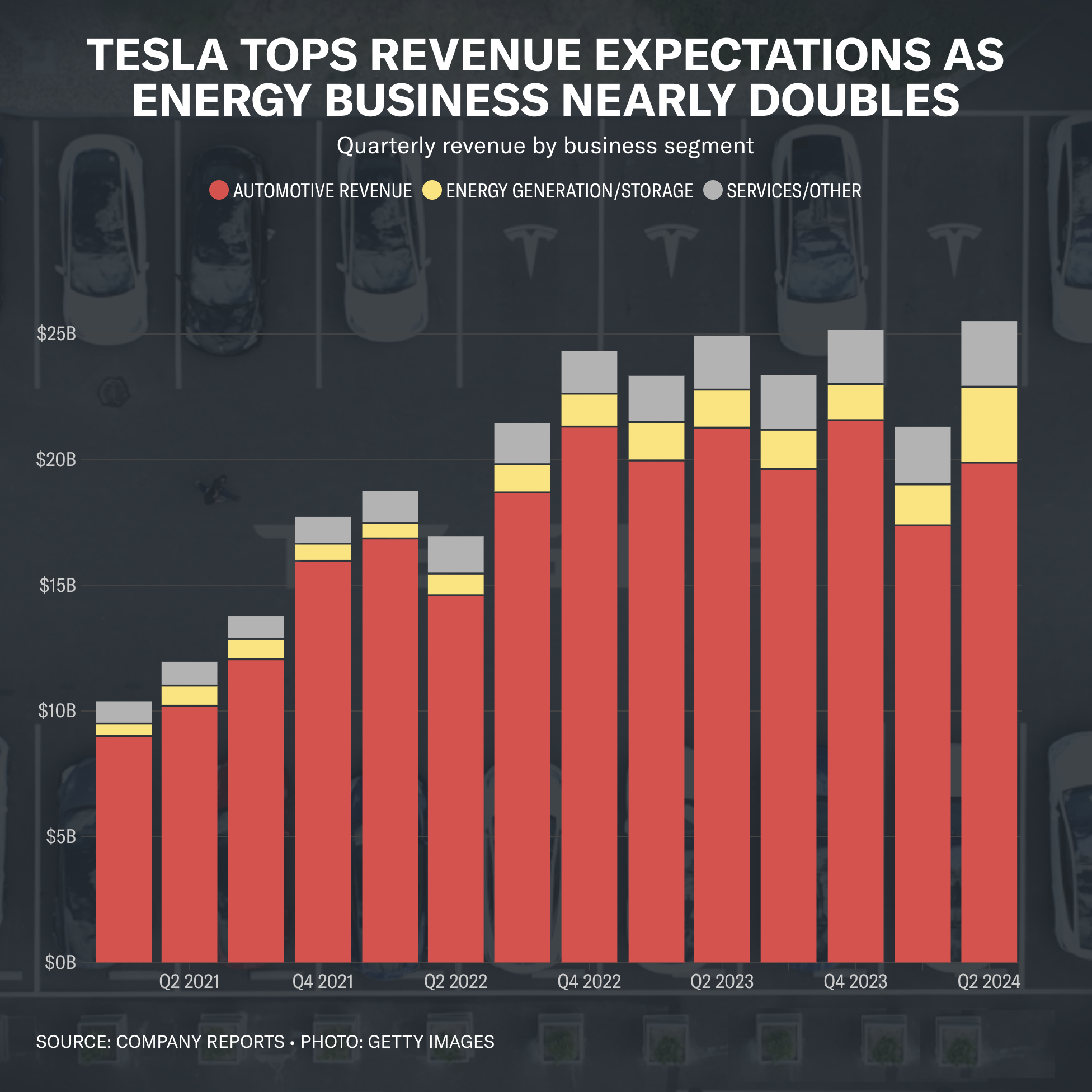

Tesla’s automotive gross margin, excluding regulatory credits, stood at 14.6% for the second quarter, falling short of the 16.29% estimate provided by analysts surveyed by Visible Alpha. According to Dan Coatsworth, an investment analyst at AJ Bell, this marks the fourth consecutive quarter in which Tesla has missed its earnings targets. Coatsworth observed that while the excitement around robotaxis, humanoid robots, and autonomous driving generates investor interest, these developments represent potential future benefits rather than immediate gains.

During a conference call, Musk pointed out that new competitors have significantly discounted their electric vehicles (EVs), which has posed a challenge for Tesla. The company’s vehicle deliveries have decreased for two consecutive quarters, as Tesla struggles with heightened competition and slow demand due to the lack of affordable new models. In particular, Tesla’s sales of EVs produced in China, which are also exported to Europe and other regions, saw a decline in the second quarter compared to the previous year. In contrast, Chinese automakers like BYD Co reported strong sales growth.

Looking ahead, Tesla anticipates a sequential increase in production for the third quarter. The company reported revenue of $25.50 billion for the second quarter, a slight increase from the previous year and above analyst expectations, according to LSEG data. Tesla also saw its sales of regulatory credits nearly triple to a record $890 million, as traditional automakers purchase these credits to meet clean-vehicle production targets. Despite this, Tesla’s net income dropped to $1.48 billion for the second quarter, down from $2.70 billion a year earlier. Adjusted earnings of 52 cents per share missed the Wall Street consensus estimate of 62 cents.

Tesla’s stock has surged more than 30% since June 13, following the approval of Musk’s $56 billion pay package, which had previously been invalidated by a Delaware court. The rise in shares has been partly fueled by investor enthusiasm for the Robotaxi project. Over the years, Musk has positioned Tesla as a technology company, with a strong focus on self-driving technology. While past predictions for the maturity of this technology have not materialized, Musk has projected that Tesla’s self-driving software will be capable of operating vehicles without human supervision by next year. He expressed confidence that this goal will be met, barring any unforeseen issues.

Tesla also indicated that the timing for the deployment of its Robotaxi will depend on technological progress and regulatory approvals. Musk, however, does not believe that regulatory hurdles will be a significant barrier. He expects Tesla to gain regulatory approval for its “supervised” Full Self-Driving software, which requires driver attention, in China and Europe by the end of the year. The unveiling of the Robotaxi has been rescheduled to October 10 from August 8 to accommodate important modifications. Musk had initially set the August date after reports that Tesla had shifted its focus from developing a new, affordable car to self-driving taxis.

David Wagner, head of equity and portfolio manager at Aptus Capital Advisors, commented on Musk’s tendency to present bold visions, but noted that these ideas often face challenges in execution. Musk had previously stated that Tesla aimed to mass-produce a robotaxi without a steering wheel or pedals by 2024. Meanwhile, General Motors announced that its Cruise self-driving unit will now focus on developing a next-generation Chevrolet Bolt, while delaying its planned Origin vehicle, which was also designed to lack a steering wheel.

In addition, Tesla reported that its Cybertruck production remains on track to become profitable by the end of the year. The company has begun validation of its first prototype Cybertruck vehicles using a new battery manufacturing technology known as dry coating, which represents a significant cost reduction milestone. Production of the Cybertruck is expected to launch in the fourth quarter, reflecting Tesla’s continued innovation and commitment to advancing its electric vehicle lineup.